Buyer's Guide

How Much Tax Do You Pay When You Sell Land? Capital Gains Explained

Owning a piece of land that sits unused can feel like a financial drain — property taxes arrive every year, the land earns nothing, and selling it is rarely as simple as listing a house. When a landowner finally decides to sell, one of the first questions that surfaces is: how much of that money will actually stay in my pocket?

The answer depends on several factors: how long the land was owned, what was originally paid for it, the seller's income level, and the state where the property sits. For those who inherited land — an extremely common situation — there is a specific IRS rule that can dramatically reduce the tax bill, sometimes to zero. This article explains the key concepts in plain terms so landowners can move forward with realistic expectations.

_______________________________________________________________________________________________________________________

What Are Capital Gains — and Why Do They Apply to Land?

A capital gain is the profit made when a capital asset sells for more than what was paid for it. Land qualifies as a capital asset, which means any profit from selling it is subject to capital gains tax.

The formula is simple:

Capital Gain = Sale Price − Cost Basis

The cost basis is what was originally paid to acquire the land — the purchase price plus closing costs or legal fees directly tied to the purchase. If land was bought for $40,000 and sold for $100,000, the capital gain is $60,000.

According to IRS Topic 409, nearly all assets held for investment — including vacant land — are classified as capital assets subject to these rules.

_______________________________________________________________________________________________________________________

Short-Term vs. Long-Term Capital Gains: A Critical Difference

The IRS taxes capital gains differently based on how long the property was held before selling:

Short-term (held one year or less): Taxed at ordinary income rates — the same rates that apply to wages, as high as 37% (IRS Topic 409).

Long-term (held more than one year): Taxed at significantly lower preferential rates.

The holding period distinction can make a substantial difference. Waiting past the one-year mark before closing a sale is often worth considering.

_______________________________________________________________________________________________________________________

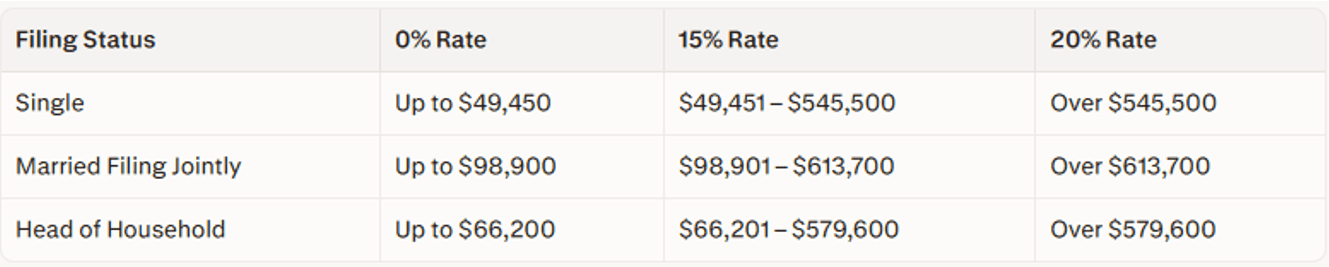

2026 Long-Term Capital Gains Tax Rates

For land held longer than one year, federal long-term capital gains rates for 2026 are 0%, 15%, or 20%, depending on total taxable income. According to Bankrate and NerdWallet, the 2026 brackets are:

|

|---|

Most landowners will fall into the 15% bracket. Higher-income sellers should also be aware of the Net Investment Income Tax (NIIT) — an additional 3.8% surtax on investment gains for individuals with adjusted gross income above $200,000 (or $250,000 married filing jointly), per the IRS.

_______________________________________________________________________________________________________________________

The Stepped-Up Basis: A Major Tax Benefit for Inherited Land

For landowners who inherited property rather than purchased it, one IRS rule deserves special attention: the stepped-up basis.

What "Stepped-Up Basis" Means

When someone inherits land, the IRS resets the cost basis to the fair market value of the land on the date the original owner died — not what that person originally paid years or decades ago. This rule is established under Internal Revenue Code Section 1014.

In practical terms: if a parent bought rural land in 1985 for $8,000, and it was worth $120,000 at the time of their death, the heir's cost basis becomes $120,000. Any appreciation that occurred during the parent's lifetime is not taxable to the heir.

Why This Matters

If an heir sells the land for close to fair market value shortly after inheriting it, the taxable gain may be very small — or zero. According to the IRS, the basis of inherited property is generally the fair market value on the date of the decedent's death.

Key points:

Selling soon after inheriting can minimize or eliminate capital gains tax, because little appreciation has occurred since the step-up date.

A proper appraisal at the time of inheritance documents the stepped-up basis. Without it, the IRS can challenge any basis claimed (University of Nebraska Center for Agricultural Profitability).

Jointly owned property: only the decedent's share receives the step-up unless community property rules apply.

Real estate qualifies for a stepped-up basis; inherited IRAs and retirement accounts do not.

_______________________________________________________________________________________________________________________

State Taxes: An Often-Overlooked Layer

Federal tax is only part of the picture. Most states also tax capital gains. According to SmartAsset, a majority of states treat capital gains as ordinary income, with state rates ranging from roughly 2.9% to over 14%. States with no income tax — including Texas, Florida, and Nevada — do not impose an additional state-level capital gains tax on a land sale.

Out-of-state sellers should confirm their specific state's rules with a tax professional before closing.

_______________________________________________________________________________________________________________________

How to Report a Land Sale to the IRS

Selling land triggers two standard federal filing requirements:

Form 8949 (Sales and Other Dispositions of Capital Assets): Itemizes each transaction — property description, acquisition date, sale date, sale price, cost basis, and resulting gain or loss (TaxAct).

Schedule D (Form 1040): Summarizes totals from Form 8949 and determines overall capital gain or loss for the year (TurboTax).

Sellers expecting a large gain may also need to make estimated tax payments during the year to avoid underpayment penalties (IRS Topic 409).

_______________________________________________________________________________________________________________________

The 1031 Exchange: Deferring Taxes by Reinvesting

Landowners who want to reinvest rather than cash out can defer capital gains tax through a 1031 exchange — named after Section 1031 of the Internal Revenue Code. This allows proceeds from a land sale to roll into a qualifying "like-kind" replacement property, postponing the tax bill.

Vacant land qualifies, provided it was held for investment purposes rather than personal use (Realized1031.com). The core requirements per Deferred.com:

Replacement property must be identified within 45 days of the sale.

The purchase must close within 180 days.

A qualified intermediary must hold the funds — the seller cannot receive the proceeds directly.

The replacement property must be of equal or greater value.

A 1031 exchange defers taxes; it does not eliminate them. Anyone considering this route should engage a tax professional before listing the land for sale.

_______________________________________________________________________________________________________________________

Why Land Can Take Longer to Sell Than Expected

Vacant land draws a narrower buyer pool than residential homes. Raw land is harder to finance — traditional mortgages rarely apply — which limits the number of qualified buyers. Properties can sit on the market for months or years while property taxes continue to accumulate.

For landowners who inherited a rural parcel far from where they live, managing a sale remotely adds further complexity: coordinating visits, navigating local regulations, and paying ongoing holding costs.

Companies like MPL Land Investing specialize in buying land directly from owners, with cash offers, no real estate agent commissions, and no closing costs charged to the seller. For out-of-state or remote owners, the entire transaction can be completed online.

_______________________________________________________________________________________________________________________

Frequently Asked Questions

Q: Do I have to pay capital gains tax if I sell inherited land?

It depends on your stepped-up basis. If the land's value has not increased significantly since the date of inheritance, the taxable gain may be very small or zero. If the land has appreciated, tax is owed on the gain above the stepped-up basis (IRS).

Q: What is the difference between short-term and long-term capital gains on land?

Land held one year or less is taxed as ordinary income — up to 37%. Land held more than one year qualifies for long-term rates of 0%, 15%, or 20%, which are significantly lower for most sellers (IRS Topic 409).

Q: How do I establish my cost basis for inherited land?

The cost basis is generally the fair market value of the land on the date the previous owner died. An appraisal obtained at the time of inheritance is the most reliable documentation (University of Nebraska Center for Agricultural Profitability).

Q: Are there state taxes on top of federal capital gains tax?

In most states, yes. Rates range from under 3% to over 14%. States without income tax — including Texas, Florida, and Nevada — impose no state-level capital gains tax (SmartAsset).

Q: What IRS forms do I need to file after selling land?

Sellers file Form 8949 to detail the transaction and Schedule D (Form 1040) to report the gain or loss — both submitted with the annual federal return (TaxAct).

Q: Can capital gains tax on a land sale be avoided entirely?

Full avoidance is rare. Heirs who sell quickly after inheritance at or near fair market value may owe little or nothing due to the stepped-up basis. A 1031 exchange can defer taxes indefinitely by reinvesting into qualifying replacement property (Realized1031.com). A tax professional can identify the best approach for a specific situation.

_______________________________________________________________________________________________________________________

This article is for educational purposes only and does not constitute tax or legal advice. Landowners should consult a qualified tax professional before making decisions about a land sale.

About MPL Land Investing

MPL Land Investing is a family-owned company that buys and sells vacant land. We work directly with landowners to provide fair, transparent deals, offering cash purchases, flexible timelines, and thoughtfully marketed properties for buyers—no commissions, no pressure, and a smooth process from start to finish.

Let's Connect

Follow us @MPLLandInvesting

Vacant Lots for Sale

Active

$19,999

▪️

2.8

Acres

0 Mill Creek Road, Warrior, AL 35810

Melanie Palmer Lozano

+1 (305) 510-1343

Active

$19,999

▪️

2.8

Acres

0 Mill Creek Road, Warrior, AL 35810

Melanie Palmer Lozano

+1 (305) 510-1343

Active

$19,999

▪️

2.8

Acres

0 Mill Creek Road, Warrior, AL 35810

Melanie Palmer Lozano

+1 (305) 510-1343

What's Your Land Worth?

Request a Cash Offer

Offers vary based on property location, size, and market conditions.